[Pammy Jaiswal and Mahak Agarwal are with Vinod Kothari & Co]

The concepts of senior management (‘SM’) and senior managerial person or personnel (‘SMP’ or ‘SMPs’) was not present under the regime established by the Companies Act, 1956, and it was first introduced in section 178 of the Companies Act, 2013 (the ‘Act, 2013’). The law requires the nomination and remuneration committee to establish the compensation policies of SMPs. The definition under the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (the ‘LODR’) issued by the Securities and Exchange Board of India (‘SEBI’) has, over time, been aligned with that under the Act, 2013. These definitions have been around for almost 10 years now, and therefore, largely seem to have settled.

However, the SEBI (Listing Obligations and Disclosure Requirements) (Second Amendment) Regulations, 2023 (issued on 14 June 2023) (the ‘LODR Amendments’) have introduced several new information requirements and obligations pertaining to SMPs. This has given rise to a need to relook at the said position from a fresh perspective.

Given the fact that the amendments specify newer and stricter obligations and disclosure norms for SMPs, it becomes imperative for companies to revisit the following matters:

- Determining who are currently designated as SMPs; and

- Identifying, with a new perspective, the persons who shall explicitly fall under this definition;

and accordingly, attract the applicability of various requirements as discussed hereinbelow.

Our detailed FAQs on the LODR Amendments can be viewed here.

The Concept of Senior Management under the Act, 2013

The scope of law revolving around ‘senior management’ under the Act, 2013 is limited. It discusses the meaning of, and the manner of appointment and removal of, SMPs.

Meaning

The term ‘senior management’ under the Act, 2013 means personnel of the company who are members of its core management team, excluding board of directors, comprising all members of management one level below the executive directors, including the functional heads.

Appointment, Removal and Remuneration of SMPs

Section 178 of the Act, 2013 requires the nomination and remuneration committee to be responsible for identifying persons who may be appointed in senior management and are also required to recommend to the board their appointment or removal. Further, the law also provides emphasis on formulation of requisite criteria for ensuring balance between fixed and incentive pay with respect to the remuneration payable to SMPs.

Definition and Meaning of SMPs

Regulation 16 of the LODR defines senior management as under:

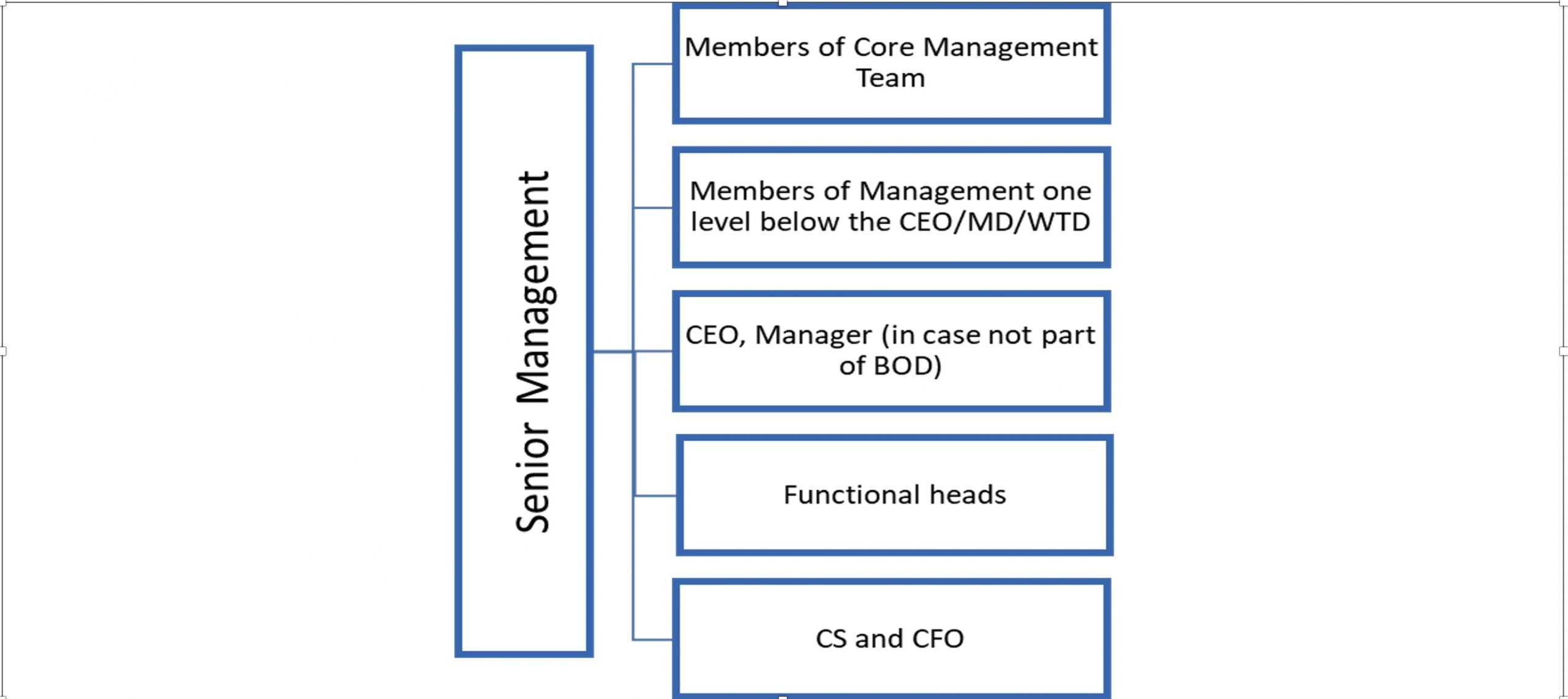

“Senior management” shall mean the officers and personnel of the listed entity who are members of its core management team, excluding the Board of Directors, and shall also comprise all the members of the management one level below the Chief Executive Officer or Managing Director or Whole Time Director or Manager (including Chief Executive Officer and Manager, in case they are not part of the Board of Directors) and shall specifically include the functional heads, by whatever name called and the Company Secretary and the Chief Financial Officer”

Accordingly, following are the inclusions and exclusions in the definition:

Inclusions

- Members of core management team;

- All members of the management one level below the chief executive officer (‘CEO’), managing director (‘MD’), or wholetime director (‘WTD’);

- CEO, manager (in case not part of the board of directors);

- Specifically include functional heads; and

- Company secretary and chief financial officer (‘CFO’).

Exclusions

- Board of Directors

On a reading of the aforesaid definition of SMP, it is understood that the same is an inclusive definition and, therefore, the actual identification of SM in a company will depend on several factors, like the meaning and participants of core management group, members falling under one level below the board, and the organizational hierarchy. For defining the officers falling under ‘core management group’ one may consider the members of the promoter group taking part in the crucial management discussions, in case there is a formal committee/ group to that effect. As regards the members falling under ‘one level below the board’ is concerned, the ones who report to the MD/ CEO or officers responsible for general management of the company would be regarded as an inclusion in the said category.

Understanding ‘Core Management’ and ‘Functional Heads’

Generally speaking, core management would mean members of the management responsible for core business functions of the organization.

Core Management

To further understand who shall fall under the ambit of core management, reference may be taken from Singapore Guidelines on Individual Accountability and Conduct applicable to Financial Institutions (regulated by Monetary Authority of Singapore), which provides a list of persons to be included in ‘core management functions’. The list includes CEO, CFO, Chief Risk Officer, Chief Operating Officer/Head of Operations, Chief Information Officer/Chief Technology Officer/Head of Information Technology, Chief Information Security Officer/Head of Information Security, Chief Data Officer, Chief Regulatory Officer, heads of business functions, head of actuarial/appointed actuary/certifying actuary, Head of Human Resources, Head of Compliance, Head of Financial Crime Prevention, and Head of Internal Audit.

Similarly, the Ministry of Economic, Trade and Industry, Japan in its Revised CGS Guidelines has laid emphasis on the composition and delegation of powers to ‘top management’. It provides an indication on the nature of work done and the members falling under the said category which includes president, CFO, CXO, etc.

Functional Head

Business functions are the activities carried out by an enterprise: they can be divided into core functions and support functions. Core business functions would mean those functions which yield income for an enterprise and these functions generally make up the primary activities of the enterprise. These would normally include operations, marketing, finance, and compliance and could otherwise vary based on the nature of the enterprise. Support business functions are ancillary (supporting) activities carried out by the enterprise to permit or to facilitate the core business functions, its production activity. These activities may include distribution and logistics, IT services, technical services, etc.

However, in the context of defining SMPs, what shall be relevant are the heads of the core functional departments of the company who report directly to the MD or WTD and the ancillary or supporting heads shall be disregarded while interpreting the definition of SM. On a joint reading of the aforesaid discussion on core management as well as functional head, it becomes clear that senior persons from ancillary or support services may form part of the core management; however, the same need not be categorized under functional head for the purpose of these regulations.

Example to Understand Core Management Team and Functional Heads

For a large-scale organization, the identification becomes even more crucial since a liberal interpretation of the meaning would involve a number of employees under the said definition and, thus, lead to several implications as discussed below. To understand the same, consider an example of K Ltd, which has several plant locations around the country with plant heads controlling the functions at each plant. All the plant heads report to the head of operations as well as the CFO. Further, the said company has around 15 functional departments, out of which 12 are main line functions and the rest are ancillary to one of the main functions. Every main line function has a functional head, and the ancillary functions have controllers reporting to the one of the functional head of the main line function. The heads of the main line functions report to the MD of K Ltd.

In the given case, if we take a close look at the definition of SM, then the following should be the result of the identification of SMs in K Ltd:

- Plant heads – Not an SM since they report to head of operations, therefore, not falling under one level below the board.

- Heads of main line functions – Should be categorised as an SM since they fall under one level below the board

- Controllers of ancillary functions – Not an SM since they report to head of main line functions.

Understanding the Implications

On SM Personnel

The amended regulations along with the existing regulations applicable to SMs impose the following obligations on them:

1. SMs are required to act with operational transparency while also maintaining confidentiality of information [regulation 4(2)(f)];

2. They are required to disclose to the board all material, commercial and financial transactions in which they have personal interest and which may lead to potential conflict of interest with the listed entity at large [regulation 26(5)]. Here, conflict of interest relates to:

- Dealing in shares of listed entity;

- Commercial dealings with bodies, which have shareholding of management and their relatives;

3. SPs shall also be required to affirm compliance with code of conduct of senior management on an annual basis [regulation 26(3)];

On Listed Companies

- Fraud by SM [Clause 6 of Para A of Part A of Sch III]

The definition and implications of being identified as an SM under the amended regulations is very wide and it is, therefore, likely that the companies may not consider covering several persons under its ambit. Fraud with respect to SM has been inclusively defined to also mean fraud under regulation 2(1)(c) of Securities and Exchange Board of India (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003 which itself has a very wide scope. The same covers wide range of activities including misrepresentation of truth, concealment of material facts, a suggestion as to an untrue fact, active concealment of fact in knowledge of the person making such representation, promise made without intention of performing it, reckless/careless representation, any act or omission which law declares as fraudulent, deceptive behavior, false statement, misinformation about securities that affects market price of such securities.

Having said that, companies which take a liberal interpretation of the definition of SM and, accordingly, keep a long list of such persons, might have to keep constant track of such activities being undertaken by their SM which, goes without stating, is a cumbersome task. Furthermore, such cases of fraud have been classified as deemed material event under regulation 30 read with Para A Part A of Schedule III, which will have to be reported by the company to the stock exchange within 12 or 24 hours, as the case may be.

- Default by SM [Clause 6 of Para A of Part A of Sch III]

The meaning of ‘default’ with regard to SM shall be seen in the following light:

- non-payment of the interest or principal amount in full on the date when the debt has become due and payable; and

- such default which has impact on the listed entity.

Further, such defaults by SM, pursuant to the recent amendments, shall be considered a deemed material event and accordingly required to be disclosed to the stock exchange within 12 hours of such default coming into notice.

- Change in SM [Clause 7 of Para A of Part A of Sch III]

Pursuant to recent amendments, change in SM shall now be a deemed material event under regulation 30 read with Para A Part A of Schedule III. In addition, the particulars of SM along with changes therein since the close of the previous financial year shall also be required to be disclosed by the company in its corporate governance report.

- Resignation of SM [Clause 7C of Para A of Part A of Sch III]

The amended LODR requires companies to disclose to the stock exchange the letter of resignation as given by the concerned SM along with detailed reasons for such resignation within seven days from the date such resignation comes into effect.

Such resignation letters carry a grave potential for the outgoing SM to negatively portray the image of the company. Accordingly, identification of SM personnel becomes of immense relevance.

- Announcement/Communication through Social Media Intermediaries or Mainstream Media by SM [Clause 18 of Para A of Part A of Sch III]

It is stated by the recent amendments that if the SMPs of the listed entity make any announcement or communication through social media intermediaries or mainstream media and such information is material in terms of regulation 30 and is not already made available in the public domain by the listed entity, the same shall be deemed to be a material event under Para A Part A of Schedule III and consequently required to be disclosed to the stock exchange.

Conclusion

In essence, the existing LODR deals with several provisions revolving around SM, imposing several disclosure norms on the company and on the SM as well. Considering these disclosures include some very sensitive areas, an immediate step for companies now will be to take a close re-look and identify the personnel that fall in this comprehensive definition in such a manner that enhanced compliances in relation to such personnel, as brought about by the recent amendments are being adequately adhered to without any adverse implications on the listed entity.

– Pammy Jaiswal & Mahak Agarwal

Leave a comment