[Vinod Kothari and Sikha Bansal are at Vinod Kothari & Company and can be reached at resolution@vinodkothari.com]

The amendments to the Insolvency and Bankruptcy Board of India (Liquidation Process) Regulations, 2016 (“Liquidation Regulations”), introduced on 28 March 2018 by incorporating a change in regulation 32 of the Liquidation Regulations, made it explicitly possible for the liquidator to transfer a company in liquidation as a going concern.

One of the authors has elaborately written on the meaning of a going concern and the issues inherent in transfer of a company as a going concern in liquidation in a post titled “Liquidation Sale as Going Concern: The concern is dead, long live the concern!”

However, realising that in circumstances there may be enormous advantages in transferring the entity as a going concern, a liquidator has to consider practical ways to enable a going concern sale in liquidation, as there are several aspects concerning settlement of liabilities from sale proceeds. The following is an attempt to draw a potential outline of a going concern sale in liquidation. It is hoped that this post is read as a sequel to the earlier one (as indicated above).

Key distinguishing features of a Going Concern Sale

Prima facie, liquidation is the anti-thesis of going concern. In liquidation, the metaphor of putting the company on its death-bed has been used. The creditors have already taken the call to close down the business and liquidate the entity. However, as we have discussed in the earlier post, there has been a series of rulings of courts about sale of a company as a going concern in liquidation, primarily motivated by the objective of keeping employment potential and economic activities intact.

Some of the key distinguishing features of a going concern sale are as follows:

|

Points of distinction |

Liquidation sale | Going concern sale |

| Retention of Business as going concern | Only to the extent required for beneficial liquidation |

May be retained, if intent is to transfer the business as a going concern. |

| Dissolution of legal entity | Legal entity gets dissolved once the liquidation is complete |

Legal entity should continue and be transferred to the acquirer. |

| Sale of assets by piecemeal sale | Liquidator has the right to cause the sale in piecemeal way, or a slump sale |

There might be several undertakings, which may be sold separately. However, the question of a piecemeal sale of an undertaking does not arise. |

| Discharge of employees | Liquidation order amounts to automatic discharge of employees |

The going concern decision is taken by the liquidator after liquidation process has been initiated. Therefore, the discharge would have happened here as well. However, in order for smooth transition to the acquirer, the employees may be re-engaged. |

Advantages of a Going Concern Sale

A going concern sale may have several advantages. At the outset, it is a sale of the entire undertaking – hence form the viewpoint of value preservation, the method works well. Quite likely, the acquirer who acquires the undertaking will have a smooth transition, as it works with the existing template.

Most importantly, there are numerous soft and intangible assets in every company. These include leases, licenses, concessions, trademarks, registrations, contracts and vendor registrations. All of these are reduced to zero value if the entity is taken into liquidation. On the contrary, as the legal entity survives in a going concern sale, the value of the above intangibles will be preserved. There would have been value in form of the benefit of carry forward of losses in accordance with the Income-tax Act, but presumably that will not be allowed to be carried forward in view of the change of control.

In toto, a going concern sale helps achieving synergy as the collective value of the assets (taking them with a view to generate future potential returns) would be higher than salvage value of assets disposed separately.

How to make a Going Concern sale work?

Prominent concerns which arise in a going concern sale are: identification of undertakings which can be sold on a going concern basis, valuation of such undertakings (i.e. assigning going concern value) and settlement of liabilities, including encumbered debt, and dues of workmen/employees, operational creditors, etc.

It may be noted that all components of a legal entity might not be crucial to effectuate a going concern sale. Hence, the liquidator should explore options and permutations and combinations to identify all undertakings that can be sold as going concern and those that should be sold separately in view of marketability, demand, feasibility, and value maximisation. A distinction may be drawn as to entire assets of the entity being called either business assets (undertakings) or non-business assets. In view of the same, there can be a sale of a business asset, i.e. an undertaking on a going concern basis. While valuation is a separate aspect, we would focus on the concern regarding liabilities, which again is intimately connected to the valuation itself. So far as liabilities are concerned, it may be possible to see the practical way of making a going concern sale work by examining what happens in a normal liquidation method.

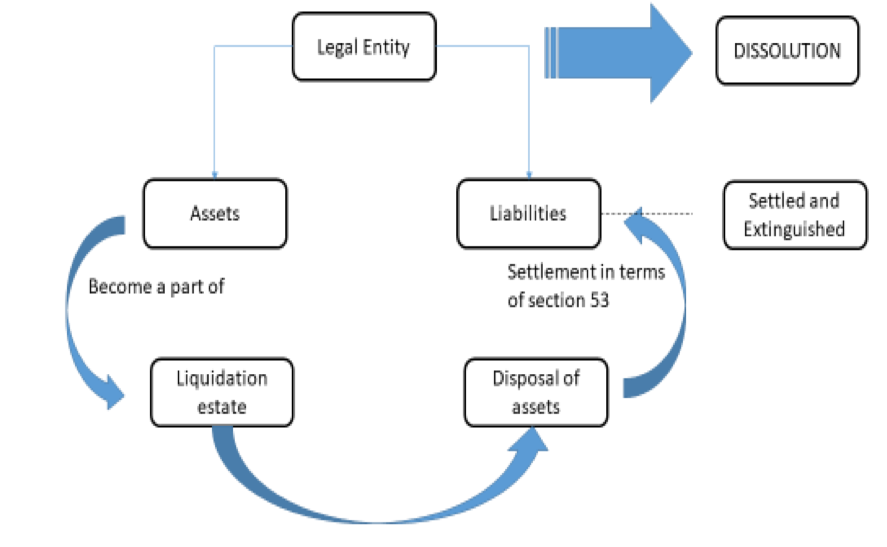

In a normal liquidation method, the assets become a part of the so-called liquidation estate. These assets, whether collectively or separately or in a set, are sold. The realisations are then distributed to the stakeholders in terms of the priorities envisaged under section 53 of the Insolvency and Bankruptcy Code, 2016 (the “Code”). Once, the pool is exhausted, the liquidator files an application for dissolution of corporate debtor. And, so far as the liabilities are concerned, the part unsettled under section 53 is automatically extinguished, as the maximum possible value out of the liquidation estate has already been extracted.

Figure 1: Normal Liquidation Method

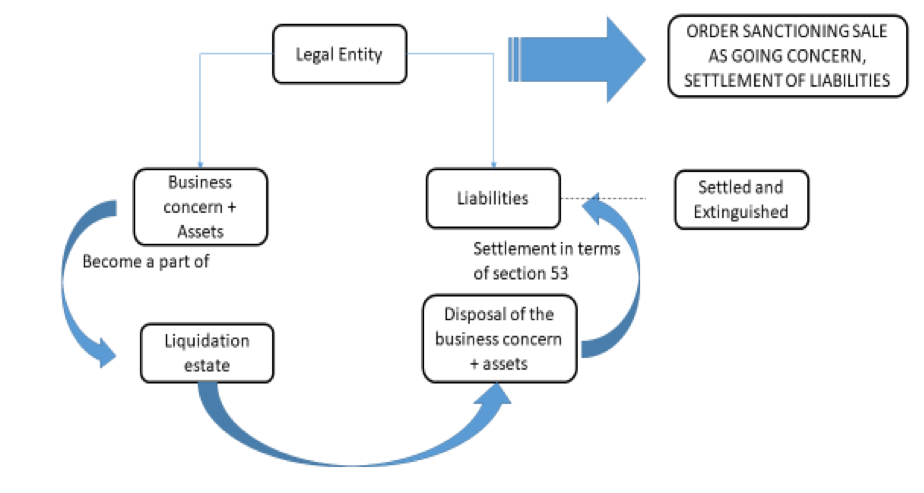

In a going concern sale, the company as a legal entity will itself be a part of the liquidation estate. All the assets of the company are still a part of the liquidation estate. A general feature of going concern sale is transfer of liabilities along with transfer of assets. However, a going concern sale in liquidationhas to be distinguished from a going concern sale in general. In a going concern sale in liquidation, there cannot be a question of the liabilities being a part of the undertaking, as that will be a case of business transfer, and not a case of liquidation. In bankrupt liquidation, there has to be a case of settling the liabilities in the priority order listed in section 53.

Hence, the business of the company as well as its assets becomes part of the liquidation estate. The legal entity continues and gets transferred to the acquirer. The proceeds realised by transfer of both of these are used by the liquidator to settle the claims, in the manner provided in section 53.

Figure 2: Going concern sale in liquidation

As to the consideration payable by the acquirer, the same is dependent on the reserve price determined in terms of regulation 35 of the Liquidation Regulations. The consideration which the acquirer pays to acquire the business concern and its assets will be split into share capital and liabilities, based on a capital structure that the acquirer decides. To the extent of the share capital, there will be an issuance of shares by the legal entity being transferred. This cannot be a case of transfer of existing shares, as existing shareholders become claimants in the process of liquidation, though they are the last in the waterfall provided in section 53.

In jurisdictions like United Kingdom, in normal circumstances, when a business changes owners, its employees may be protected under the Transfer of Undertakings (Protection of Employment) Regulations (popularly referred to as “TUPE”). However, where the employer is insolvent and the business is being transferred or taken over by another company, the protection employees get is different from in a normal transfer. In a TUPE-protected transfer, the new employer must pay any amount left over after employees have been paid from the government’s national insurance fund. The employees are unlikely to be protected under TUPE if the business is closing down. But, TUPE regulations will normally apply if it is being rescued and taken over or transferred. However, there can be variations in the terms and conditions of the employment, if it prevents job losses. Any changes, which should necessarily be compliant with statutory employment rights, must be agreed with employee or trade union representatives.

What happens to the encumbrances on the assets?

On sale as a going concern, a question may arise as to whether the encumbrances which existed on the asset prior to the sale shall pass on with the entity to the acquirer. The liquidator does not have much of the role where the secured creditors decide to realise the security interest all on their own. However, where the security interest is relinquished, there is no question of passing of the encumbrances on the assets of the entity.

Order of Adjudicating Authority

In a normal liquidation, there is an order of the adjudicating authority, on completion of the liquidation, for dissolution. Since there is no dissolution in the case of a going concern sale, there may have to be an order pertaining to sanction of sale as going concern, the issue of shares, settlement of all existing claims and liabilities pertaining to the period up to the completion of liquidation.

Use of section 230 of the Companies Act, whether possible

Under section 230 of the Companies Act, 2013, the liquidator is also one of the parties entitled to make an application for a scheme of arrangement.

Section 230 of the Companies Act, 2013 provides as follows –

(1) Where a compromise or arrangement is proposed—

(a) between a company and its creditors or any class of them; or

(b) between a company and its members or any class of them,

the Tribunal may, on the application of the company or of any creditor or member of the company, or in the case of a company which is being wound up, of the liquidator, order a meeting of the creditors or class of creditors, or of the members or class of members, as the case may be, to be called, held and conducted in such manner as the Tribunal directs.

[Emphasis added]

Though the process may be used by the liquidator to facilitate a compromise or arrangement with stakeholders like employees, workmen and operational creditors, the use of this process is not convenient – as the scheme requires a special resolution of the creditors or class of creditors with whom the compromise or arrangement is proposed, which may be difficult to obtain in liquidation.

Way ahead

While the enabling provision for sale as going concern is not something new, yet it would be interesting to see the interface between the idea and the provisions of the Code. The economy is yet to see a successful going concern sale under the Code; meanwhile the law-makers ought to keep the framework ready.

– Vinod Kothari & Sikha Bansal

Leave a comment