[The

following guest post is contributed by Nivedita

Shankar, Senior Associate, Corporate Law Division, Vinod Kothari &

Company. The author may be reached at [email protected]].

following guest post is contributed by Nivedita

Shankar, Senior Associate, Corporate Law Division, Vinod Kothari &

Company. The author may be reached at [email protected]].

An increase in the threshold limit for foreign

investment in insurance companies has been hailed as a major thrust for the

insurance sector, which has seen very few players. In this background, the Indian Insurance Companies (Foreign Investment) Rules, 2015

(‘Rules, 2015’) were issued by way of Notification

No. G.S.R. 115(E) dated February 19, 2015 with the intention of providing

regulatory clarity on shareholding pattern in Indian insurance companies.

However, Rule 4 of Rules, 2015 has posed a vital question for Indian insurance

companies – how to ensure compliance with Rules, 2015? As has been discussed

further in this post, the very intent behind issuance of Rules, 2015 was to

ensure that Indian insurance companies are always owned and controlled by resident

Indian citizens. In fact, the Insurance Laws (Amendment) Act, 2015 also amended

the definition of Indian insurance company to allow only 49% of foreign investment,

which meant that the rest of the shareholding was to be with Indians. However

Rule 4 of Rules, 2015 has played a complete dampener in this regard. Where the

idea pursuant to amendment of FDI Policy and Insurance Laws (Amendment) Act,

2015 is clear that Indian insurance companies have to be under the control of

resident citizens, Rule 4 of Rules, 2015 is creating an additional requirement by

requiring Indian insurance companies to look one layer up and see the actual ownership

and control behind the resident Indian citizen.

investment in insurance companies has been hailed as a major thrust for the

insurance sector, which has seen very few players. In this background, the Indian Insurance Companies (Foreign Investment) Rules, 2015

(‘Rules, 2015’) were issued by way of Notification

No. G.S.R. 115(E) dated February 19, 2015 with the intention of providing

regulatory clarity on shareholding pattern in Indian insurance companies.

However, Rule 4 of Rules, 2015 has posed a vital question for Indian insurance

companies – how to ensure compliance with Rules, 2015? As has been discussed

further in this post, the very intent behind issuance of Rules, 2015 was to

ensure that Indian insurance companies are always owned and controlled by resident

Indian citizens. In fact, the Insurance Laws (Amendment) Act, 2015 also amended

the definition of Indian insurance company to allow only 49% of foreign investment,

which meant that the rest of the shareholding was to be with Indians. However

Rule 4 of Rules, 2015 has played a complete dampener in this regard. Where the

idea pursuant to amendment of FDI Policy and Insurance Laws (Amendment) Act,

2015 is clear that Indian insurance companies have to be under the control of

resident citizens, Rule 4 of Rules, 2015 is creating an additional requirement by

requiring Indian insurance companies to look one layer up and see the actual ownership

and control behind the resident Indian citizen.

Provisions

of Rules, 2015

of Rules, 2015

Rule 3 of Rules, 2015 states that:

No Indian insurance company shall allow the aggregate holdings by

way of Total Foreign Investment in

equity shares held by Foreign Investors,

including portfolio investors, to exceed forty-nine percent, of the paid up

equity capital of such Indian insurance company.

way of Total Foreign Investment in

equity shares held by Foreign Investors,

including portfolio investors, to exceed forty-nine percent, of the paid up

equity capital of such Indian insurance company.

Rule 4 of Rules, 2015 states that:

An Indian Insurance Company

shall ensure that its ownership and control shall remain at all times in the

hands of the resident Indian entities referred to in clauses (k) and (l) of

rule 2.

shall ensure that its ownership and control shall remain at all times in the

hands of the resident Indian entities referred to in clauses (k) and (l) of

rule 2.

To juxtapose the two Rules stated

above, where on one hand Rule 3 allows total foreign investment to the tune of

49% of the paid up equity capital of Indian insurance companies, Rule 4 on the

other hand prescribes that only Indian resident citizens can control and own

the Indian insurance companies. Looking at the definition of ‘Indian Ownership

of an Indian Insurance Company’[1] and

‘Indian Control of an Indian Insurance Company’[2] in

Rules, 2015 what transpires is that even if foreign investment is capped at

49%, the rest of the investment has to be in the hands of resident Indian

citizens which basically means that they have to be owned by Indians. Hence,

where on one hand foreign investment is not allowed beyond 49%, on the other

hand ownership and control is allowed by only such companies that are owned by

Indians. This rules out the possibility of Indian insurance companies being

owned and controlled by such companies that may have been incorporated in India

but are ultimately foreign controlled. Hence Rule 4 prescribes a requirement

that is beyond what was actually envisaged.

above, where on one hand Rule 3 allows total foreign investment to the tune of

49% of the paid up equity capital of Indian insurance companies, Rule 4 on the

other hand prescribes that only Indian resident citizens can control and own

the Indian insurance companies. Looking at the definition of ‘Indian Ownership

of an Indian Insurance Company’[1] and

‘Indian Control of an Indian Insurance Company’[2] in

Rules, 2015 what transpires is that even if foreign investment is capped at

49%, the rest of the investment has to be in the hands of resident Indian

citizens which basically means that they have to be owned by Indians. Hence,

where on one hand foreign investment is not allowed beyond 49%, on the other

hand ownership and control is allowed by only such companies that are owned by

Indians. This rules out the possibility of Indian insurance companies being

owned and controlled by such companies that may have been incorporated in India

but are ultimately foreign controlled. Hence Rule 4 prescribes a requirement

that is beyond what was actually envisaged.

Further, similar to

the Consolidated FDI Policy, the Insurance Regulatory and Development Authority

of India (‘IRDA’) has also prescribed the method for calculating the direct and

indirect investment in Indian insurance companies. Since by virtue of para

4.1.4 of Consolidated FDI Policy, insurance companies are not subject to

calculation of direct and indirect foreign investment as prescribed therein,

one has to refer to IRDA (Registration of Indian Insurance Companies) (Seventh

Amendment) Regulations, 2000 (the ‘Regulations 2000’) which is yet to be

published in the Official Gazette. Regulation 11 prescribes the method for

calculation of direct and indirect holding of equity capital held by foreign

investors as follows:

the Consolidated FDI Policy, the Insurance Regulatory and Development Authority

of India (‘IRDA’) has also prescribed the method for calculating the direct and

indirect investment in Indian insurance companies. Since by virtue of para

4.1.4 of Consolidated FDI Policy, insurance companies are not subject to

calculation of direct and indirect foreign investment as prescribed therein,

one has to refer to IRDA (Registration of Indian Insurance Companies) (Seventh

Amendment) Regulations, 2000 (the ‘Regulations 2000’) which is yet to be

published in the Official Gazette. Regulation 11 prescribes the method for

calculation of direct and indirect holding of equity capital held by foreign

investors as follows:

1. the

quantum of paid

up equity share

capital held by

the foreign investors including

foreign venture capital investors, in the applicant company; and

quantum of paid

up equity share

capital held by

the foreign investors including

foreign venture capital investors, in the applicant company; and

2. the proportion of the paid up equity

share capital held or controlled by such foreign investors in the Indian

promoters or Indian Investors as mentioned in sub- clauses (i) of this sub

regulation.

share capital held or controlled by such foreign investors in the Indian

promoters or Indian Investors as mentioned in sub- clauses (i) of this sub

regulation.

Reading Rule 4 of

Rules, 2015 and 7th Amendment to Regulations, 2000, the following two

scenarios can be envisaged:

Rules, 2015 and 7th Amendment to Regulations, 2000, the following two

scenarios can be envisaged:

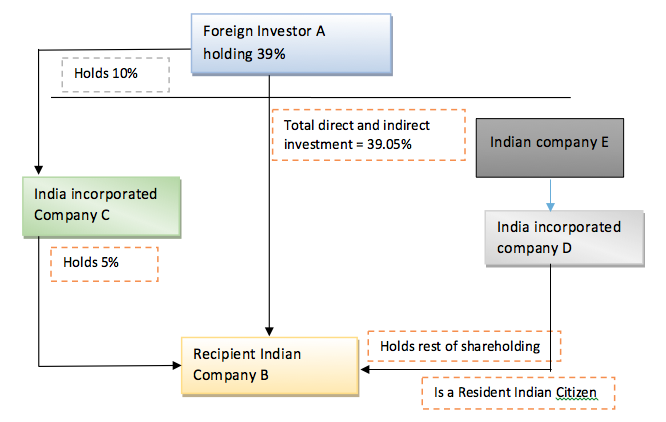

Exhibit 1

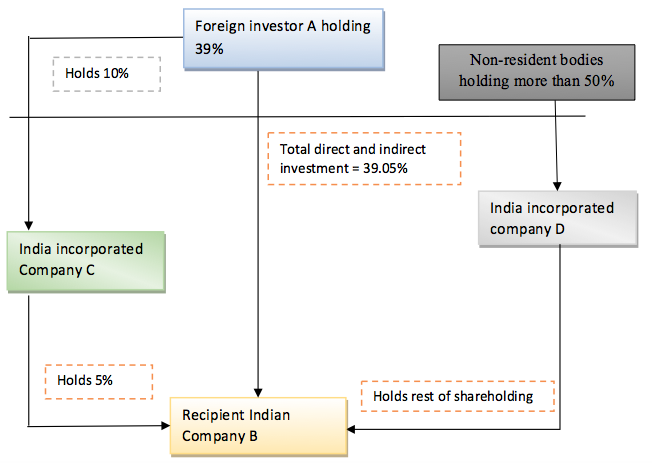

Exhibit 2

Analysis

We now analyse the effect of Exhibit

1 and Exhibit 2 in light of Rule 4 of Rules, 2014:

1 and Exhibit 2 in light of Rule 4 of Rules, 2014:

|

If the Indian Company D is owned and controlled by resident

Indian citizens |

If the Indian Company D is incorporated in India but

not owned and controlled by resident Indian citizens |

|

Evidently from Exhibit 1 it is clear that more than

50% of the total paid up capital of Indian insurance company is held by Indian resident citizen. Hence compliance with Rule 4 is not an issue. Also, since the non-resident body corporate is holding less than 49%, provisions of Rule 3 are also met. |

This is a case of Foreign Owned and Controlled

Companies (‘FOCC’) which are subject to the provisions of Consolidated FDI Policy, 2015. Going by the definition of Foreign Investors[3] in Rules, 2015, it is clear that FOCCs do not qualify to be Foreign Investor.

Hence owing to the fact that any FOCC is not owned

and controlled by resident Indian citizen, for the purpose of Rule 4 of Rules, 2015, any FOCC cannot invest more than 49% in the Indian insurance company. Hence what will constitute 49% is holding of Foreign Investors + FOCC.

This leaves Indian insurance company in a very

peculiar position. This is because the rest of 51% will have to be mandatorily held by resident Indian citizens only. Hence Indian insurance company having a structure similar to Exhibit 2 will have to rethink their shareholding pattern. |

Thus

there is an obvious disconnect in the way Rule 4 has been drafted. The intent

was of course to ensure that insurance companies in India are owned and

controlled by Indians. However this has led to Rule 4 being drafted in such a

way that it unintentionally imposes additional compliance burden for Indian

insurance companies. The way Rule 4 has been drafted, it also hints at lack of

regulatory clarity on what should be the actual shareholding pattern of Indian

insurance companies. Thus even if it is clear that foreign investment cannot be

more than 49%, clarity regarding Indian investment is also required at the

earliest.

there is an obvious disconnect in the way Rule 4 has been drafted. The intent

was of course to ensure that insurance companies in India are owned and

controlled by Indians. However this has led to Rule 4 being drafted in such a

way that it unintentionally imposes additional compliance burden for Indian

insurance companies. The way Rule 4 has been drafted, it also hints at lack of

regulatory clarity on what should be the actual shareholding pattern of Indian

insurance companies. Thus even if it is clear that foreign investment cannot be

more than 49%, clarity regarding Indian investment is also required at the

earliest.

–

Nivedita Shankar

Nivedita Shankar

[1] Indian Ownership of an Indian Insurance Company means more than 50 per

cent of the equity capital in it is beneficially owned by resident Indian

citizens or Indian companies, which are owned

and controlled by resident Indian citizens.

cent of the equity capital in it is beneficially owned by resident Indian

citizens or Indian companies, which are owned

and controlled by resident Indian citizens.

[2] Indian Control

of an Indian Insurance Company means control of such Indian Insurance Company

by resident Indian citizens or Indian companies, which are owned and controlled by resident Indian citizens.

of an Indian Insurance Company means control of such Indian Insurance Company

by resident Indian citizens or Indian companies, which are owned and controlled by resident Indian citizens.

[3] Foreign Investors for the purpose of Rules,

2015 means all eligible non-resident entities or persons resident outside India

investing in the equity shares of an Indian Insurance Company, as permitted to

do so through Foreign Direct Investment and Foreign Portfolio Investment under

FEMA Regulations, 2000 as described in these rules.

2015 means all eligible non-resident entities or persons resident outside India

investing in the equity shares of an Indian Insurance Company, as permitted to

do so through Foreign Direct Investment and Foreign Portfolio Investment under

FEMA Regulations, 2000 as described in these rules.

Sporadic (to share tentative reaction)

As independently understood, the premise on which the rules have been framed and founded on the latest innovative thinking that ‘equity shareholding’ and ‘controlling interest’ are two distinct , not connected or related, concepts; and are not but mutually unrelated and has to be forcibly divorced. Except that, each empowered authority has chosen to frame its own Rules but differently; and that seems to account for the fact that the rules under reference are mutually conflicting, hence confusing lending no clarity.

Is this not nothing but yet another development that juts out and bears testimony to the irreversible perpetuation, and unmindful extension , – that all started in the field of tax regime- of that very same idea,- rather than an obsession haunting/troubling the brains behind since then,- of unduly placing over-emphasis on preference to “SUBSTANCE “ over “ the "FORM”?!

Open, as ever before remain, to be enlightened!

The analysis presented for Exhibit 2 is completely wrong and misguiding. Regulation 11 states that

“1. the quantum of paid up equity share capital held by the foreign investors including foreign venture capital investors, in the applicant company; and

2. the proportion of the paid up equity share capital held or controlled by such foreign investors in the Indian promoters or Indian Investors as mentioned in sub- clauses (i) of this sub regulation.”

Only in the event that such foreign investor (the same entity investing in Point 1) holds shares in the Indian Party and if the total shareholding of such foreign investor exceeds 51% in the Indian Promoter/Indian Investor will such Indian Promoter/Investor stand in violation of Rule 4 of Indian Insurance Companies (Foreign Investment) Rules, 2015 by not being an IOCC and hence be ineligible to invest in the applicant insurance company.

Request the editors to review guest posts. This blog is well reputed and such callous analysis is unworthy of publication herein.

Sir,

The very intent behind giving Exhibit 2 was to show the anamoly of Rule 4. It is further explained in the Table below.Any FOCC is a company in which non-resident entities hold more than 50%.